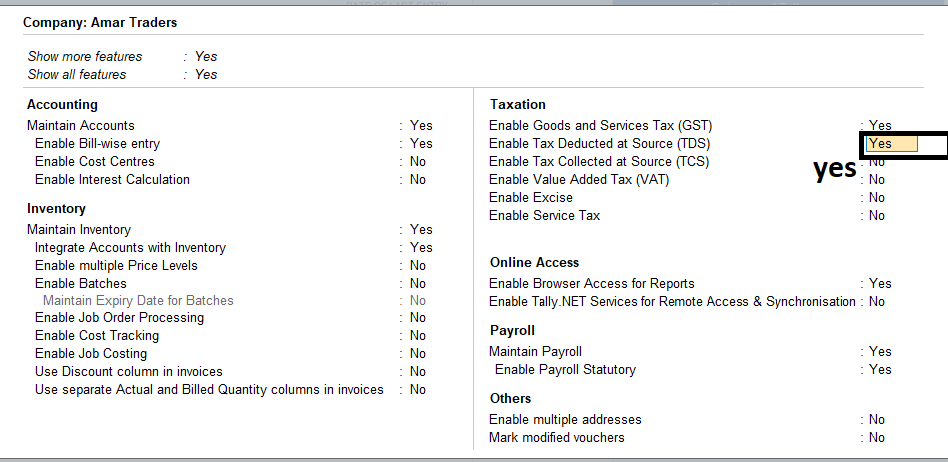

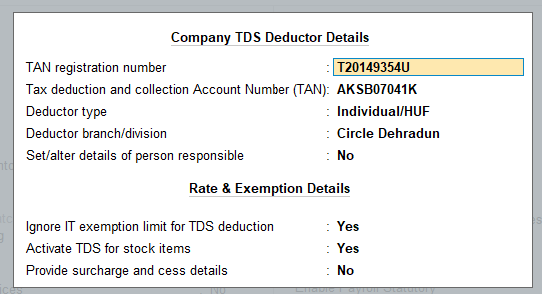

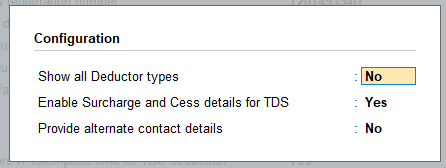

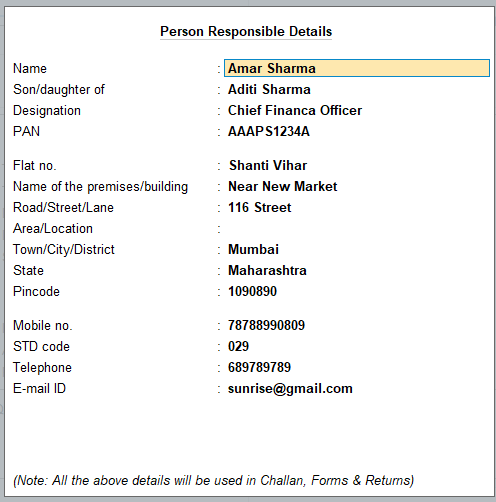

Tax deducted at Source (TDS) in Tally prime

Data Analytics and Data Science institute in Dehradun Uttarakhand

Data Analytics and Data Science institute in Dehradun Uttarakhand