Skip to content

Data Analytics and Data Science institute in Dehradun Uttarakhand

Data Analytics and Data Science institute in Dehradun Uttarakhand

Home

About Us

Course

Data science course

Data Analytics Training Course

Learning Resources

Contact Us

hire from us

Institute Gallery

Blog

Search for:

Book Now

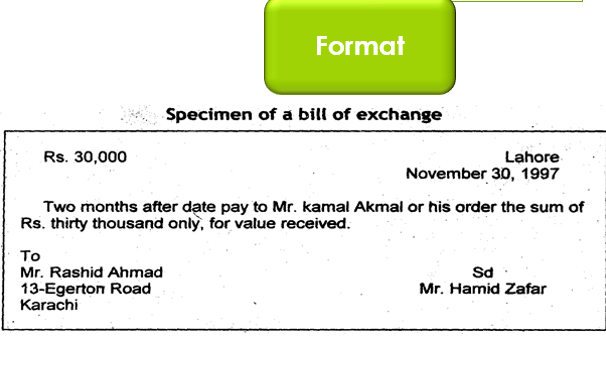

Journal Entry of Bill of Exchange in Accounting

Home

-

Accounting

-

Journal Entry of Bill of Exchange in Accounting

3

Jun, 2021

Journal Entry of Bill of Exchange in Accounting

Close this module