Prepaid Expense in Accounting and its journal Entry

What is prepaid Expense?

Prepaid expenses are those expenses that are paid in advance. It means the cost of expense is paid but they are not yet used up or incurred. Prepaid expenses are Asset by nature. The prepaid expense comes under the category of Current Assets. They are treated as current assets because most of the prepaid expense is consumed within a month or so.

If prepaid expense are not consumed with a particular financial period then they are transferred to the next financial year in the Asset side of the balance sheet under category current assets.

Examples of Prepaid Expense

Salary paid to Mohan Rs 12000 along with an advance salary Rs 4000.

Here Mohan is getting a salary of Rs 16,000 which even includes advance salary, therefore, we have to use the following concept before making a journal entry of Prepaid expense in books of accounts.

before we go further we have understood the following concept of accounting.

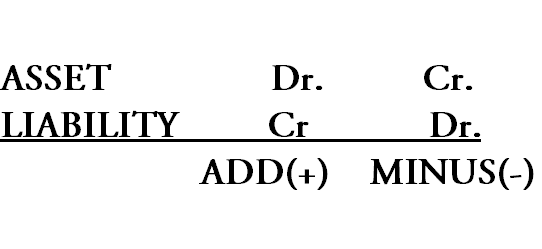

To record the entry of outstanding Expenses in books of accounts we should know that

When we ADD Assets in Business we Debit our Asset

Similarly, When we ADD Liability in Business we Credit our Liability

And When we Minus or deduct Asset in business we Credit our Asset

Similar when we Minus or deduct our Liability form business we Debit our liability

it can be more clear from the picture given below.

Now as per the above example our Assets to Rs 4000 is created in the books of accounts, therefore, we have to book our Assets by debiting it name given to the current asset can be Advance salary. The journal entry for the above in the books of accounts will be :

Journal Entry of Prepaid Expense

Salary paid to Mohan Rs 12000 along with an advance salary Rs 4000.

Salary A/c Dr. 12,000

Advance Salary A/c Dr 4,000

To cash A/c 16.000

(being salary paid with advance salary )

here Advance salary is paid in advance, therefore, it is treated as Assets under books of Accounts. when it is booked.

Example: An insurance premium paid Rs 12000 on 1 Dec 2019.

On 1 Dec 2019. the following journal entry is made.

Insurance premium A/c Dr 12,000

To Bank/Cash A/c 12000

Now at the end of the accounting year, 31 march 2020 following entry needs to be made.

Prepaid Insurance Expense A/c Dr 8000

To Insurance A/c 8000

(adjustment of prepaid insurance )

Prepaid expense under income statement and balance Sheet

Now in Final Accounts salary will be shown in the Profit and Loss A/c and Advance salary Rent will be shown in the Asset side of balance sheet

shown below Profit and Loss A/c

| Particular |

Amount |

Particular |

Amount |

| salary A/c |

12,000 |

|

|

Outstanding expense under Balance Sheet

| Liability |

Amount |

Asset |

Amount |

|

|

Advance Salary |

4000 |

Adjustment of Prepaid expense

When Advance Salary is paid

salary A/c Dr. 10,000

Advance Salary A/c Dr 4000

To cash A/c 14,000

(being salary paid with advance salary )

here we reduce our liability in the next accounting year by paying our dues.

now in next month advance salary is adjusted

Salary A/c Dr 12,000

To cash A/c 8000

To Advance Salary A/c 4000

(being salary paid with adjustment of adv. salary)

Advance expense in Trial Balance :

Outstanding expense are liability by nature and liability are shown in the credit side of Trial balance

Dr. Cr.

| Particular |

Amount |

Particular |

Amount |

| Advance salary |

4000 |

|

|