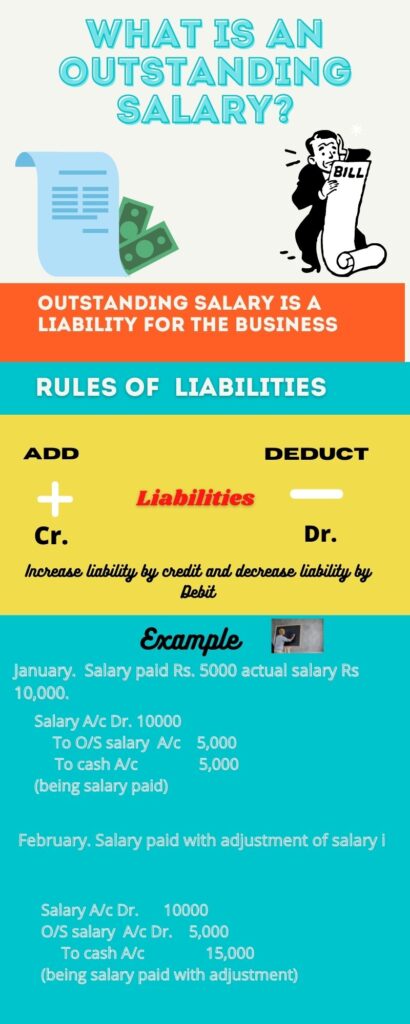

Oustanding salary is under which account?

Answer: Outstanding salary is a personal representative account. As per the matching concept, salary is due but not yet paid. So, Unpaid salary to be shown as liability under ‘Expenses Payable’ or ‘Salary Payable’ in the Balance sheet on liabilities side and on another aspect of dual entry to be placed in Profit & Loss Account.

Where Outstanding Salary appearing in Trial Balance are shown:

Answer: On the liability side of the balance sheet.Its means its already adjusted no need to shown in Profit and loss Accounts.

What is the definition of outstanding salary?

Outstanding salaries are salaries that are due and have not yet been paid.

For example, the staff of Amar Traders has worked for the month of April.

It is now the 3rd of May and they still have not been paid,

so the salaries are “payable” or “owing” or “outstanding” (all the same thing) .