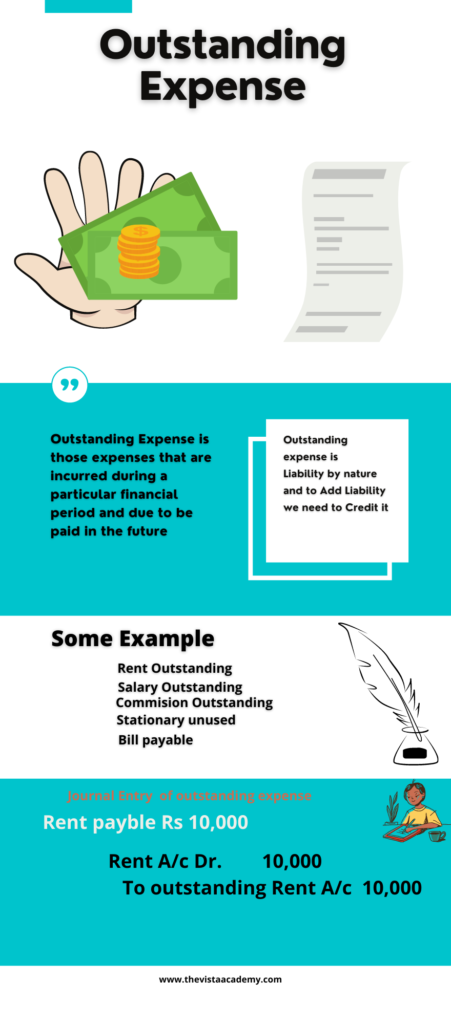

What is Outstanding Expense in Accounting ?

Example of Outstanding Expenses

Example 1.

Suppose in Financial year 1 April 2019 to 31 Dec 2020 wages paid is Rs. 11000 but the last month wages not paid Rs 1000.

Therefore wages not paid in a particular financial year are outstanding.

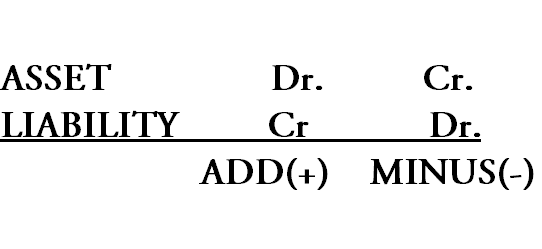

To record the entry of outstanding Expenses in books of accounts we should know that When we ADD Assets in Business we Debit our Asset Similarly, When we ADD Liability in Business we Credit our Liability And When we Minus or deduct Asset in business we Credit our Asset Similar when we Minus or deduct our Liability form business we Debit our liability ir can be more clear from the picture given below.

Now as per above example our liability to 1000 is created in the books of accounts, therefore, we have to book our liability by crediting it the journal entry for the above in the books of accounts will be